|

|

|

|

|

Week 04 -2012 | From Jan 23 to Jan 27, 2012 |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| |

Economic Data for Week 04-2012 | Global View | Week Rating

| DATE |

DAY |

REPORT/CATEGORY |

HIGHLIGHTS ON WEEK 04-2012 |

Last |

|

Mon |

Non Reports for Our Global Vision |

There will be no Economic Reports released on Monday. |

N/A |

|

|

No Reports |

|

|

|

Tue |

FOMC Meeting #1 Day 1 of 2 |

The Federal Reserve's 2 day monetary policy meeting has begun and policymakers will be explaining their Fed funds forecasts in a way that would minimize volatility. |

N/A |

|

|

Interest Rates |

The most important thing to look for tomorrow is the timing of the first interest rate increase - will it be in late 2013 or early 2014? |

|

|

Tue |

ICSC Goldman Sachs Index |

The International Council of Shopping Centers and Goldman Sachs Retail Chain Store Sales Index slipped 1.4% in the week ended Saturday from the week before on a seasonally adjusted basis. |

-1.4% W/W |

|

|

Sales and Inventories |

From the Northwest to the Northeast strong winter storms affected consumer demand this past week as it limited consumers' ability to shop. |

|

|

Tue |

Johnson Redbook |

National chain store sales fell 1.6% in the first three weeks of January from December. Sales for the week climbed 2.5% year-over-year.

|

2.5% Y/Y |

|

|

Sales and Inventories |

The Johnson Redbook Index also showed seasonally adjusted sales for the period were up 2.9% from last year, also equaling the target. |

|

|

Wed |

MBA purchase Applications |

The MBA's seasonally adjusted index of mortgage application activity, which includes both refinancing and home purchase demand, fell 5% in the week ended Jan 20. |

-5.0% W/W |

|

|

Real Estate |

Applications for U.S. home mortgages retreated last week, giving back some of the previous week's surge as interest rates rose |

|

|

Wed |

FHFA House Price Index |

U.S. home prices fell 1.8% in November from a year earlier, as foreclosures held back a recovery in property values. But M/M 1.0% increase. |

1.0% M/M |

|

|

Real Estate |

According to the FHFA, house prices in November rebounded 1.0% after declining 0.7% in October. November's number came in higher than expectations for a 0.1% decrease. |

|

|

Wed |

Pending Home Sales Index |

Pending home sales drop from 19-month high hit in November, but remain at higher level. The index of sales agreements fell 3.5 per cent last month to a reading of 96.6. M/M -3.5%. |

96.6 Level |

|

|

Real Estate |

But the reading is still the second highest since April 2010, the last month that buyers could qualify for a federal home-buying tax credit. A reading of 100 is considered healthy. |

|

|

Wed |

EIA Crude Oil Report |

Stocks of oil show a build for the 4th time in 5 weeks, up 3.6 million barrels to 334.8 million. To put pressure on Iran�s nuclear policies., EU has imposed sanctions on Iranian oil. |

3.6M Barrels |

|

|

Commodity |

Inventory and output data from the oil sector are pointing to economic weakness in what is a counter-indication compared to the bulk of indicators which are pointing to improvement. |

|

|

Wed |

FOMC Meeting #1 Day 2 of 2 |

The Federal Reserve�s said that rates could stay extremely low for another three years provides juice for risk assets like stocks, but signals more worries ahead for the economy. |

0.25% Rate |

|

|

Interest Rates |

The Fed also took the historic step of setting an inflation target of 2%, when it released its forecast. Federal Funds Rate - Target Level 0.0 to 0.25 % |

|

|

Thu |

Durable Goods Orders |

Orders for durable goods, items which last over 3 years, in the US rose 3% in December 2011. It is the fifth rise in the past six months and follows a 4.3% rise in November. |

3.0% M/M |

|

|

Manufacturing |

The latest increase could be in part attributed to aircraft orders, but even after stripping transportation products out the underlying trend has accelerated. |

|

|

Thu |

Chicago Fed Nat Activity Index |

Led by improvements in production- and employment-related indicators, the Chicago Fed National Activity Index increased to +0.17 in December from -0.46 in November.

|

0.17 Level |

|

|

Growth |

The index�s three-month moving average, CFNAI-MA3, increased from -0.19 in November to -0.08 in December-- its highest value since March 2011. |

|

|

Thu |

Jobless/Initial Claims |

Seasonally adjusted initial claims increased to 377,000 for the week ended Jan. 21. The previous week saw the lowest level for new claims in nearly four years at 356,000. |

377K Claims |

|

|

Employment |

U.S. jobless claims rise slightly, but long-term trend remains cause for optimism. However, the measure�s longer-term downward trend signals continuing improvement in the labor market. |

|

|

Thu |

New Home Sales |

Sales of new U.S. homes unexpectedly declined in December for the first time in four months, capping the slowest year on record for builders.

|

307K Level |

|

|

Real Estate |

Purchases of single-family properties decreased 2.2% to a 307,000 annual pace. Last year marked the worst year for the industry in records going back to 1963.

|

|

|

Thu |

Leading Indicators |

The U.S. index of leading economic indicators rose 0.4% in December. The Leading Economic Index, which has risen for the past seven months, climbed in December to 94.3. |

0.4% M/M |

|

|

Business Activity |

In December, the gain was widespread among the leading indicators, suggesting economic conditions should improve in early 2012. |

|

|

Thu |

Fixed Mortgage Rates |

Fixed 30-year mortgage rates averaged 4.11%, up 5 basis points from 4.06%. The Fed sees longer-term rates reaching between 4% and 4.5% |

3.91% APR |

|

|

Interest Rates |

The new commitment extends the prior statement that economic conditions were likely to keep rates at the historic low range of 0% to 0.25% until at least mid-2013. |

|

|

Thu |

EIA Natural Gas Report |

Natural gas in storage fell 192 billion cubic feet in the January 20 week to 3,098 bcf. A withdrawal of 180 bcf was expected. |

-192 bcf |

|

|

Commodity |

Despite natural gas prices falling to near 10-year lows last week demand for gas will be much higher than oil in the long term with the Asia-Pacific region driving the sector's growth. |

|

|

Thu |

Fed Balance Sheet |

The Fed's balance sheet edged up $0.1 billion after expanding $20.2 billion the prior week. "Other assets"; grew $2.2 billion. Total assets for the January 25 week stood at $2.922 trillion. |

0.1B Assets |

|

|

Government |

The advance was led by a $10.0 billion rise in holdings of Treasuries which was offset by an $11.8 billion drop in mortgage-backed securities |

|

|

Thu |

M2 Money Supply |

|

$8.1B |

|

|

Money Supply |

|

|

|

Fri |

Fixed Mortgage Rates |

Freddie Mac said Thursday the average rate on the 30-year fixed mortgage rose to 3.98% this week. That's up from 3.88% the previous week, which was the lowest level on record. |

3.98%

APR

|

|

|

Interest Rates |

The average on the 15-year fixed�mortgage�also rose to 3.24%, from 3.17% the previous week. The 15-year�mortgage�hit a record low of 3.16% two weeks ago. |

|

|

Fri |

Gross Domestic Product (GDP) |

The economy grew at its fastest pace in 1-1/2 years, but the GDP was weaker-than-expected Q4 U.S. GDP which it was +2.8% annualized versus expectations of +3.0% annualized. |

2.80% Rate |

|

|

Growth |

U.S. GDP expanded at a 2.8% annual rate, a sharp acceleration from the 1.8% clip of the prior three months. Economists expectations was a 3.0% rate, we rated positive. |

|

|

Fri |

Consumer Sentiment |

US consumer confidence rose for the second month in a row, to an eight-month high in December. One reason for the rise in sentiment has been steady improvement in the labor markets. |

75.0 Level |

|

|

Consumer |

The University of Michigan preliminary January reading on its overall index of consumer sentiment rose to 74.0 from 69.9 in December for the fifth month of gains and the highest level since May 2011. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

Glossary: |

|

Current Week |

|

Chart View |

|

Positive View |

|

Negative View |

|

Flat View |

|

Non Available |

|

| |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

| |

|

| WEEK 04-2012 ENDING JAN. 27 |

Reports Commentary

Both Redbook and ICSC-Goldman say heavy weather has been holding down sales so far this month.

The MBA's seasonally adjusted index of refinancing applications slipped 5.2%, while the gauge of loan requests for home purchases was off 5.4%.

The National Association of Realtors (NAR) pending home sales index fell 3.5% month-over-month. The number of Americans who signed contracts to buy homes fell in December after hitting the highest level in a year and a half a month earlier.

The increase in contract signings is another indication that the troubled housing market improved at the end of last year going into 2012. further gains would be needed to reduce the millions of unsold foreclosed homes sitting idle on the market.

The price of light crude, supported by supply issues tied to Iran and not by prospects of strengthening demand, is up about 50 cents to the $98.50 area.

The Fed now sees GDP growth between 2.2% and 2.7% for 2012, down from 2.5 to 2.9%, and 2013 growth of 2.8 to 3.2%, down from 3% to 3.5%. Federal Funds Rate - Target Level 0.0 to 0.25 % .

The Federal Open Market Committee said Wednesday that the long-term inflation goal is 2%, as measured by the annual change in the price index for personal consumption expenditures.

The Fed also forecasts GDP growth between 2.2% and 2.7% this year, an unemployment rate between 8.2% and 8.5% and PCE inflation between 1.4% and 1.8%.

Manufacturing is picking up steam as December durables were strong and above expectations.

The threat of further price declines in home sales may be dissuading some Americans from buying a new home even with mortgage rates near all-time lows and more people finding work.

we won't see a meaningful increase as long as new homes are competing with those existing homes. Builders continue to contend with a number of existing homes that are deeply discounted.

December�s CFNAI-MA3 suggests that growth in national economic activity was slightly below its historical trend. The economic slack reflected in this level of the CFNAI- MA3 suggests limited inflationary pressure from economic activity over the coming year.

Weekly jobless claims were in line with expectations, rising 21,000 to 377,000 in the week ended Jan. 21. Meanwhile, December's orders for durable goods surged 3%, above estimates of a 2% gain.

The economy ended 2011 on a fairly positive note, but the composition of growth in the last quarter is not favorable for growth early this year.

The nation's gross domestic product -- the value of all goods and services produced -- grew at an annual rate of 2.8% between October and December. That is up from 1.8% growth in the third quarter and 1.3% in the second quarter. It was the fastest pace since the second quarter of 2010.

The Fed warned the economy still faced big risks, a suggestion the euro zone debt crisis could still hit hard. Expectations of soft growth led the Federal Reserve on Wednesday to say it expected to keep interest rates at rock bottom levels at least through late 2014.

The Fed is attempting to shield the economy from a potentially more severe recession in Europe. Even though the economy improved last quarter there are a number of headwinds and a lot of uncertainty surrounding Europe, emerging markets and also U.S. fiscal policy.

The weaker-than-expected Q4 U.S. GDP which it was +2.8% annualized versus expectations of +3.0% annualized. Aslo Q4 personal consumption grew +2.0%, weaker than expectations of +2.4%.

Concern the European debt crisis may worsen after credit-default swaps to insure Portuguese government debt rose to a record.

Unexpected increase in Jan U.S. University of Michigan consumer confidence to an 11-month high (+1.0 to 75.0 versus expectations of unchanged at 74.0).

169 companies in the S&P 500 that reported earnings results since Jan 9 have beaten analysts' estimates

Low demand and high inventory levels in the U.S. Natural Gas has deterred some companies from future investments

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

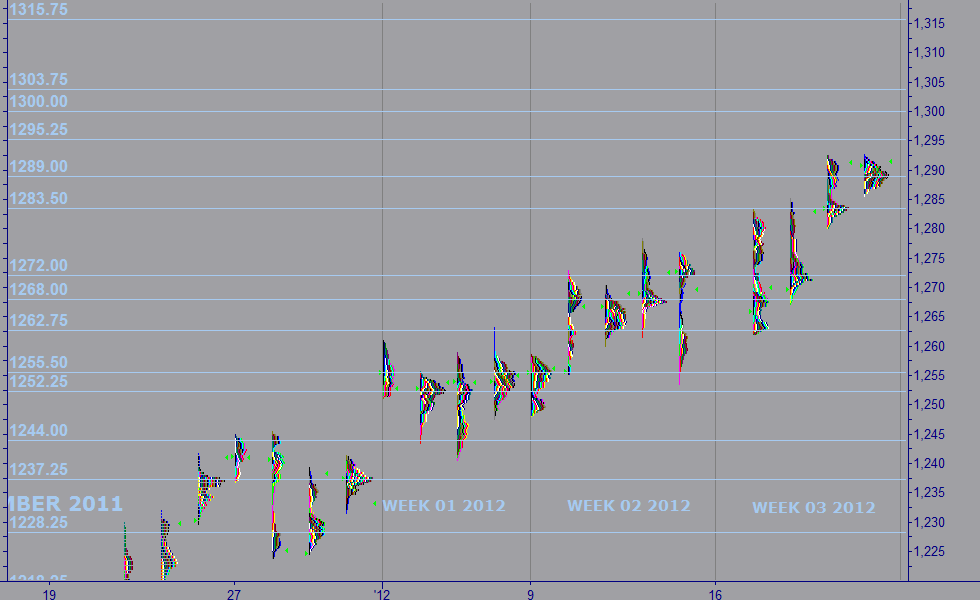

| MARKET PROFILE |

|

WEEKS 2012 |

WEEK 04 |

% FROM CLOSE |

% FROM OPEN |

|

RESISTANCE 1 |

1,315.75 |

1.88% |

1.89% |

|

RESISTANCE 2 |

1,303.75 |

0.95% |

0.64% |

|

CLOSE JAN 20 |

1,291.50 |

|

|

|

OPEN JAN 22 |

1,292.00 |

0.04% |

|

|

SUPPORT 1 |

1,289.00 |

-0.19% |

-0.24% |

|

SUPPORT 2 |

1,283.50 |

-0.62% |

-0.68% |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|

|

IMPORTANT NOTE: In an effort to comply with all applicable rules, regulations and disclosures please be so kind and read the "General Disclosure" below: |

| |

|

|

|

|

| GENERAL DISCLOSURE - TRADINGVESTING.COM |

- The material contained on our Website and Economic Calendar must be used at your own risk. Material is believed to be reliable, but we do not guarantee its accuracy or validity, nor is Tradingvesting.com responsible for any errors or omissions which may occur. The analysis and/or recommendations made by Tradingvesting.com do not provide, imply, or otherwise constitute a guarantee of performance. All contents and recommendations are based on data and sources believed to be reliable, but accuracy and completeness cannot be guaranteed. It should not be assumed that future results will be profitable or will equal past performance, real, indicated or implied.Tradingvesting.com website and material contained therein is not a solicitation to participate in the Futures/Stocks/Options Market. This Economic Calendar does not include Earning Releases, Announced Stock Splits, Upcoming Initial Public Offerings with Underwritings or Rating Changes. Tradingvesting.com has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Unless indicated otherwise: economic data is from the U.S and intraday data is at least 20 minutes delayed; all prices are in the local currency; Time is U.S. Eastern Time. Furthermore, there is a very high degree of risk involved in trading.Tradingvesting.com assumes no responsibilities for your trading and investment results, please red our Risk Disclosure.

- Tradingvesting.com does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time. All information on this website are for educational purposes only and are not intended to provide financial advice. Any statements about profits or income, expressed or implied, do not represent a guarantee. Your actual trading may result in losses as no trading system is guaranteed. You accept full responsibilities for your actions, trades, profit or loss, and agree to hold Tradingvesting.com and any authorized distributors of this information harmless in any and all ways. We respect your right to privacy, please click here to view our privacy policy.

- U.S. Government Required Disclaimer - Commodity Futures Trading Commission.

Futures and options trading has large potential rewards, but also large potential risk. You must be aware of the risks and be willing to accept them in order to invest in the futures and options markets. Don't trade with money you can't afford to lose. This website is neither a solicitation nor an offer to Buy/Sell futures or options. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed on this website. The past performance of any trading system or methodology is not necessarily indicative of future results.

- CFTC rule 4.41:Hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under-or-over compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.

- Risk Warning: Trading foreign exchange on margin carries a high level of risk, and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange trading, and seek advice from an independent financial advisor if you have any doubts. Our linking to these sites does not constitute an endorsement of any products, services or the information found on them. Once you link to another site you are subject to the policies of the new site. By using this site, you agree to the Terms of Service, Privacy Policy and Risk Disclosure. Copyright � 2012 Tradingvesting, LLC. All rights reserved. If you have any questions regarding the Online Economic Calendar application, please contact us: click here >

THIS BRIEF STATEMENT CANNOT, OF COURSE, DISCLOSE ALL THE RISKS AND OTHER ASPECTS OF THE COMMODITY MARKETS AND EQUITY MARKETS. PLEASE READ MORE AT: TERMS OF SERVICE.

|

|

|

| |

|

|

|

|

|

| |

|

|

|

|

|